Or how a few references to insurance send me down a rabbit hole, again

It will not surprise you that I read my fair share of history books. I admit, too, that any time a book mentions “insurance” I immediately get very excited about it. I recently finished Timothy Egan’s “A Fever in the Heartland: The Ku Klux Klan’s Plot to Take Over America and the Woman who Stopped Them” and, well, I wanted to share the insurance-related stuff that I found and the rabbit hole I went down as a result.

Link to the book (bear with me, I’m still figuring Substack out): Get it from your library or support a local bookstore!

Egan is a great writer though I personally don’t always connect fully with his work; I could not tell you specifically why that is, maybe it’s his writing voice. Even so, I do read and recommend his stuff to other people, and this book is no exception.

If you are interested at all in knowing why Indiana had one of the largest KKK memberships in the United States in the 1920s, and how the murder trial of the leader of the Klan in the Midwest led to the downfall of the Klan, well, here go you.

And if you’re like me and current events in the United States make you want to curl up into a ball at the hopelessness of it all, this book will remind you that…you could make a good argument that American has always been awful. So…buyer beware?

It’s not all awful, I promise. Subscribe!

Anyway, DC “Steve” Stephenson, the absolutely awful human “being” who led the Klan in the Midwest, was a sexual predator whose actions directly led to the death of a woman in Indiana named Madge Oberholtzer. Just before his murder trial started, however, there was a fire at Stephenson’s expensive, ornate home in Indianapolis. Conveniently, Stephenson was living in a hotel at the time and had moved a lot of his furniture out of the home the week prior.

It also turned out that there was a significant amount of gasoline and oil found at the home, leading the fire marshal to suspect that it was arson and not an accident.

The Indianapolis Times, April 17, 1925: Photo Courtesy of Newspaper Archives

The insurance part of this is a little complicated. Egan mentions in his book that the authorities automatically suspected arson. So of course, I had to go digging for more information. Who was involved in the insurance claim, how much was the claim, and what happened in the end?

Stephenson was convicted of the murder of Madge Oberholtzer and went to prison for life. His two lackeys, Earl Gantry and Earl Klenck, were charged with arson, but those charges were later dropped. (The two men were also indicted on the case involving Oberholtzer’s murder but were found not guilty, which…well, they were definitely involved.)

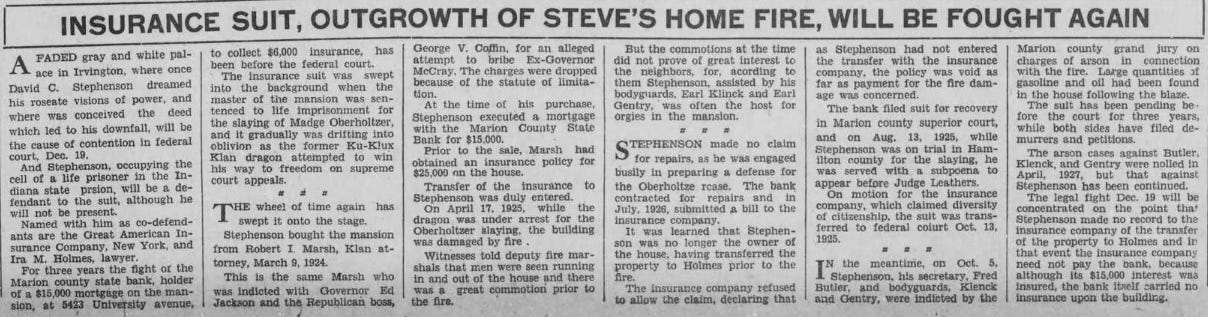

After about a half hour of poking around into different newspaper archives, I found this hidden on page 17 of the Indianapolis paper:

The Indianapolis Times, November 9, 1928: Photo Courtesy of Newspaper Archives

It’s a bit hard to read, but to summarize:

The home in Indianapolis was sold to Stephenson in 1924. The prior owner, Robert Marsh, was a crony of Stephenson’s and a Klan member. Marsh had insured the home with Great American Insurance Company for $25,000. When Stephenson bought the home, Marsh transferred the insurance policy over to him. In addition, Stephenson had a $15,000 mortgage with a local bank.

We know that Stephenson was in need of money when the trial started. You would think that the plan was to burn the house down and then make an insurance claim in the amount of $25,000, but that’s not actually what happened. Stephenson had actually “transferred ownership” of the home before the fire to Ira M. Holmes. Holmes was a lawyer, and most importantly, he was Stephenson’s lawyer in the murder trial. Was this home transfer a way of paying Holmes, who was quite a well-known defense lawyer and probably fairly pricey? I mean, it was a very nice house. But then why try to burn it down? There doesn’t appear to be any indication that Holmes was considered as a possible co-conspirator for the arson.

Either way, what made it complicated was that neither Stephenson or Holmes ever made a claim with the insurance company—the claim came from the bank, who had been the entity to actually complete the repairs. They were looking for $6,000 in reimbursement.

Great American denied the claim because they had 1. never received notice of the transfer of deed from Stephenson to Holmes and 2. because the bank had no relationship with the insurance policy—and it did not have its own insurance policy on the property. (Typically, you would add a bank to your insurance policy if you have a mortgage, but…again, the lack of detail on how the property was transferred and whether or not Holmes agreed to assume the mortgage and the insurance…it’s a mess.)

From this article we know that Stephenson was charged with arson in October of 1928, while he was already serving a life sentence for Oberholtzer’s murder. In addition, the bank took Great American, Stephenson, and Holmes to court which appeared to be ongoing as of the writing of this article in 1928.

Unfortunately, after this the trail went cold for me. I would really like to find out what happened with this case, and I would particularly like to see the argument Great American made and the policy forms. It appears that the National Archives may have some records related to this case in their facility in Chicago, which…is not that far for a day trip. If I make it out there and find something more, I will let you know.

By the way, Ira M Holmes has an absolutely bizzare history, after the Stephenson case, and so I’ll leave you with this:

The Evening Gazette, Xenia, Ohio February 7, 1928: Photo Courtesy of Newspaper Archives

Until later,

Meredith